U.S. Firearms Industry

Today Report – 2025

Innovation, Responsiveness Vital To Success

Image created by Adobe Photoshop

Once again, the U.S. firearms industry finds itself at a crossroads. We survived the pandemic and two contentious presidential election cycles over the past five-plus years. But what now?

Here in 2025, fear-based buying isn’t going to be a factor for today’s consumer. In fact, with inventory largely replenished, consumers have an abundance of options on where they can choose to spend their money. It’s going to be fine margins that determine whether or not a customer makes a purchase in today’s market.

A focus on product innovation, developing new ways to reach customers, using data to stay engaged with market conditions and expanding the joy of the shooting sports and hunting to customers represent sound investments.

One way to look at where we’re going is to look at where we’ve been — which brings us to this year’s “U.S. Firearms Industry Today” report, featuring a comprehensive look back to ATF’s annual firearms production data and other international insights. Let’s dig in.

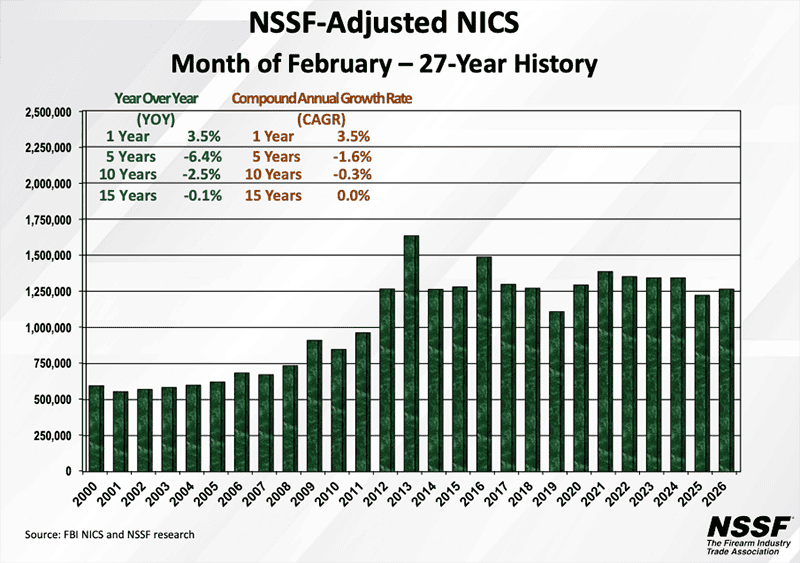

Current NICS Trends

Though not a direct correlation to firearms sales, NSSF-adjusted NICS data provides an additional picture of current market conditions.

From Jan. 1 to May 31, 2025, NSSF-adjusted NICS background checks totaled 6,063,240 — the eighth-highest tally in the system’s history through the first five months of a year. With the exception of January, each month in 2025 has trailed its 2024 counterpart. The year-over-year (YOY) decrease in NSSF-adjusted NICS checks stands at 3.6% (from 6,288,066 to 6,063,240).

There are positives to take away from the current market conditions, especially when placing it in a historical context. For example, the total observed through the first five months of this year isn’t too far away from 2016 (6,179,528). At the time, this was the second-highest total recorded through the first five months of the year. In 2019, the year before the world changed, the first five months of the year represented the nadir of NICS checks during Trump’s first term in office (5,317,913).

Incredibly, the streak of 1 million NSSF-adjusted NICS checks per month that began Aug. 2019 has continued through May 2025 — a span of 70 consecutive months. From Jan. 2000 to July 2019, this figure was eclipsed only 67 times. Not to mitigate current challenges, but this provides another frame of reference to where our industry stands today.

NICS Background Checks: NSSF-Adjusted (Jan. 2021–May 2025)

NSSF removes NICS purpose codes used by several states for CCW application checks and other purposes. The removal of this data provides a more accurate report of background checks conducted for the purchase of firearms. Visit nssf.org/research.

Ruger To Focus On “Innovation”

Two of the three largest U.S. firearms manufacturers in 2023, Ruger and Smith & Wesson, are publicly traded. The companies’ quarterly earnings releases provide additional context to understand current market conditions.

In January, Ruger announced President and CEO Chris Killoy would be retiring from his role on March 1, 2025, transitioning to a short-term special advisor to incoming President and CEO Todd Seyfert. Killoy will remain on the Ruger board.

Seyfert’s industry experience includes serving as CEO of FeraDyne Outdoors and holding key leadership roles at ATK/Vista Outdoor, Magnum Research, Bushnell, Michaels of Oregon and Birchwood Laboratories.

April 30, Ruger announced its Q1 2025 net sales totaled $135.7 million — a fractional decrease (-0.8%) from the corresponding period in 2024, when net sales were $136.8 million.

Sales of new products — including the RXM pistol, Super Wrangler revolver, Marlin lever-action rifles and American Centerfire Rifle Generation II — represented $40.7 million (31.6%) of firearm sales for Q1 2025.

As of March 29, Ruger’s cash and short-term investments totaled $108.3 million and the company has no debt. Seyfert shared how Ruger is fighting to address current market headwinds.

“The challenges in the firearms market are clear and well-documented across the industry. According to RetailBI’s Q1 2025 report, retail firearm unit sales declined 9.6% year-over-year, with revenue down 11.5%. Handguns, rifles and shotguns were all under pressure, and even adjusted NICS checks declined by 4.2%,” he noted. “Despite these two headwinds, I’m proud to report that Ruger remained flat in sales, while staying profitable. My mindset as CEO is although the firearms industry may be cyclical, Ruger does not have to be, and our performance this quarter supports that.”

To this end, Ruger is focusing on innovation to drive consumer interest. Recent partnerships with Magpul (RXM) and Dead Air Silencers (RXD Series of suppressors) are representative of the company’s intent.

June 13, Seyfert marked his 100th day at Ruger by disseminating an internal memo to Ruger employees to update them on short- and long-term plans for the company. (The memo was made public via an 8-K filing with the U.S. Securities and Exchange Commission.)

In the memo, Seyfert detailed several key initiatives — such as product repositioning (bringing in products at lower price points, in line with market conditions), leadership transition costs (evolving Ruger’s leadership structure and right-sizing its Connecticut operations), organizational realignment and inventory rationalization — would incur $15–20 million in expenses for the remainder of the year, but would set the company up for stability and profitable growth in the long term.

“None of this will slow our momentum when it comes to investing in what matters most, including aggressive new product development and expansion of capacity in areas where market demand exceeds our current ability to supply,” he wrote. “We remain fully committed to profitable expansion, product innovation, agile responsiveness and ensuring we meet the expectations of our customers and the marketplace.”

Smith & Wesson Q4 2025 Results

June 18, Smith & Wesson reported its Q4 and full fiscal 2025 financial results. Net sales for the quarter totaled $140.8 million, a decrease of $18.4 million (-11.6%) from the comparable 2024 quarter. Full year fiscal 2025 net sales totaled $474.7 million, down $61.2 million (-11.4%) from the prior fiscal year.

Mark Smith, S&W president and CEO, cited “macroeconomic and industry trends” as sources behind diminished returns during the quarter.

“While the combination of lower sales and production volumes, along with mix factors, pressured margins, we were able to partially offset the bottom-line impact through disciplined cost management and by leveraging our flexible manufacturing model,” he said. “Looking at the overall firearms market, we continue to see consumers generally being cautious due to macroeconomic factors pressuring discretionary spending.”

Smith anticipates continued constraints in the near term.

“While new products and lower price point offerings are still performing well, overall conditions suggest headwinds will likely persist in the near term. Despite these challenges, we remain well-positioned to succeed in this environment,” he said.

Deana McPherson, S&W executive VP and CFO, noted while market conditions have been challenging, new products have stabilized the company’s performance.

“We believe that firearm market conditions have been negatively impacted by persistent inflation, high interest rates and uncertainty caused by tariff concerns. That being said, the success of our new products has enabled us to maintain a leadership position in the categories of the firearm market in which we compete,” she noted.

Looking ahead, McPherson expects demand to remain steady but constrained by ongoing economic pressures.

“We currently expect demand for firearms in fiscal 2026 to be similar to what we saw in fiscal 2025, remaining subject to economic headwinds such as inflation and the impact of tariff-related cost increases,” she concluded.

7 Insights From 2023 Firearms Production, 2023–2024 Import Data

Earlier this year, ATF released its 2023 Annual Firearms Manufacturing & Export Report (AFMER) — the most recent data available. (There’s a one-year delay in reporting to comply with the Trade Secrets Act, so 2025 production data will not be publicized until 2027.)

To avoid confusion, these figures comprise the number and types of firearms produced and sold, distributed or exported into commerce. (Military contracts are excluded.) This data is not a 1:1 representation of market share at the counter, but there is a correlation, of course.

Additionally, AFMER data does not record firearms imported into the U.S. — which has grown into a significant segment of the U.S. firearms landscape. A second data set used in this SI report comes from the U.S. Census Bureau, which identifies the countries of origin and types of firearms imported into the U.S., rather than specific brands.

U.S. Firearms Production (2004–2023)

1. 15.5% Drop-Off, In Context

Looking back to 2023, the industry’s cyclical nature was on full display once again. After producing 10,013,895 firearms in 2022 (only the fourth time the industry has passed the 10 million plateau), there were 8,466,729 manufactured in 2023. Year-over-year, this drop was “only” 15.5%.

The industry is no stranger to wild annual swings, both positive and negative. Since 2013, U.S. firearms production YOY comparisons have oscillated quite a bit: 25.1%, -16%, 2.5%, 19.7%, -29%, 5.2%, -20.2%, 53.3%, 28.6%, -20% and 15.4%. In that span, single-digit percentage changes occurred only twice.

Widening the span a further 10 years (2004–2023), single-digit changes took place five times. It’s little wonder why both Ruger and Smith & Wesson have highlighted their “flexible manufacturing” models in recent public filings.

Total U.S. Firearm Production (2004–2023)

*Editor’s Note: ATF published a revision of its 2022 AFMER data mid-June 2024. SI used the original 2022 AFMER data set, published in Jan. 2024, in its reporting for the July 2024 issue. The updated report included an additional 191 FFLs, explaining the slight variance in the totals published in last year’s issue. This chart has been updated to reflect the revised 2022 figures from ATF.

2. The Top 5

With 1,304,628 firearms in 2023, Ruger was the top U.S. manufacturer for the second year in a row. It has held this title for seven of the past 10 years. Ruger wasn’t the top producer in any single category in 2023, but was the second-largest rifle maker and third in pistol and revolver manufacturing. While its overall YOY figures were down 16.5% (from 1,562,014 to 1,304,628), Ruger did record a slight increase in its revolver production (from 174,947 to 177,366).

After soaring into the top two U.S. firearms manufacturers in 2022, SIG SAUER retained its ranking in 2023. It was the only other U.S. gunmaker to cross the 1 million mark (1,001,916) in 2023 — buoyed by its impressive pistol production (944,562), which accounted for 94.2% of its overall firearms production. No surprise, SIG was the top 9mm pistol producer — a rank it has held each year since 2018.

Smith & Wesson was the third-largest U.S. firearms manufacturer in 2023, totaling 991,565 firearms. With 196,279 revolvers, S&W was the top maker in that category.

Savage Arms was the fourth-largest firearms maker, a ranking it also achieved in 2023. Its long-gun production (721,314) topped the charts for the second year running. In rifles, Savage achieved 5.1% YOY growth (from 608,579 to 639,591).

Rounding out the top five U.S. firearms manufacturers, Henry Repeating Arms jumped two spots from number seven in 2022 to number five in 2023. Henry has been a steady presence in the top 10 U.S. firearms manufacturers over the past decade. According to our records, this is the first time Henry has broken into the top five. Notably, Henry entered the wheelgun market in 2023, launching the Big Boy Revolver, chambered in .357 Mag./.38 Spl. Producing 5,223 revolvers, Henry ranked as the 10th largest revolver maker.

3. The Top 40’s Performance

As noted in previous reports, there is a significant amount of consolidation at the top of the U.S. firearms manufacturing pyramid. Together, the 40 largest U.S. manufacturers produced 7,817,539 firearms in 2023 — 92.3% of all firearms produced in the U.S. that year. In 2022, the top 40 producers accounted for 92.9% of all firearms.

Manufacturers that did not rank in the top 40 in 2022 but did in 2023 were: Anderson Mfg., Armscor USA, Axon Enterprise, DC Machine, North American Arms and Wilson Combat.

DC Machine, which is owned by JJE Capital (owners of Palmetto State Armory), did not report any firearms production in 2022, but has been a prominent gun barrel and barrel extension producer since it was established in 2004.

North American Arms has been a mainstay in the top 40 U.S. manufacturers over the years and rebounded nicely in 2023. The company produced 60,343 firearms in 2023, more than five-and-a-half times its 2022 total (10,768). Its 2023 total surpasses what it achieved in 2020 (51,192) and 2021 (57,836).

Armscor USA’s domestic production is kicking into high gear. The company produced 28,086 revolvers and 12 pistols in 2023 (its Cedar City, Utah, facility opened in 2022).

Wilson Combat’s annual growth nearly doubled, from 16,932 in 2022 to 30,423 in 2023.

Top 40 U.S. Firearms Manufacturers (2023)

4. U.S. Handgun Production

U.S. firearms manufacturers produced 4,744,571 handguns in 2023, down 18.8% from its 2022 total (5,843,030). Examining longer-term trends, however, paints a rosier picture. For example: Compared to the pre-pandemic era, the 2023 handgun tally trails only 2013 and 2016.

For the pistol category, there were declines in each of the major calibers — with the exception of the “To .25” category, which posted an 8.9% increase over 2022’s total (from 122,679 to 133,643).

9mm continued its recent dominance of the pistol segment — accounting for 60.3% of all pistols produced in 2023. That equates to three out of every five pistols produced in 2023 were in 9mm. This proportion is higher than what was observed in 2022, when 9mm pistols constituted 56.5% of total pistol production.

YOY revolver production posted a small percentage drop (-3.1%) — from 830,786 in 2022 to 805,054 in 2023. Despite the overall decline, three of the six caliber categories posted increases over 2022: .32, .357 and .44.

A bonus for our online readers: the U.S. Handgun Production, Pistol Production and Revolver Production charts have been expanded to reveal more manufacturers than what we had space for in the printed issue. Keep scrolling to glean additional insights.

U.S. Handgun Production (2023)

Total includes all U.S. handgun manufacturers.

U.S. Pistol Production (2023)

Total includes all U.S. manufacturers.

U.S. Revolver Production (2023)Total includes all U.S. revolver manufacturers.

Total includes all U.S. revolver manufacturers.

5. U.S. Long-Gun & Misc. Firearms Production

Like handguns, overall U.S. long-gun production contracted in 2023 — falling from 4,168,169 in 2022 to 3,722,158 (-10.7%). Of the 15 top U.S. long-gun manufacturers, six posted increases in 2023: Savage Arms, Ruger, Henry, S&W, Palmetto State Armory and Legacy Sports.

In rifles, the YOY decrease was 11% (from 3,505,818 to 3,119,376). Over the past 20 years, this total ranks as the eighth-most prolific year for rifle manufacturing. (Rifle manufacturing peaked at 4,239,335 in 2016.)

Shotgun production dropped 8.9% (from 662,350 to 602,782). Over the past 20 years, shotgun production has gradually fallen — the 2023 total represents the fourth-lowest since 2004. (2018–2020 represent the bottom three.)

With 253,633 shotguns in 2023, O.F. Mossberg/Maverick Arms was the top U.S. shotgun manufacturer for the seventh year in a row. Its YOY shotgun production dipped slightly (-4.8%, from 266,382) but its rifle manufacturing jumped from 74,309 to 77,085 (3.7%).

Not included in the overall firearms production and export totals, SI began reporting on U.S. miscellaneous firearms production in 2017. In 2022, this category dramatically expanded by nearly 70% to 2,171,255. In 2023, misc. firearms production dropped to 1,305,530 — which ranks as the second-highest total since 2017. By some distance, the top three 2023 producers in the misc. firearms category were Anderson Mfg., Palmetto State Armory and Aero Precision.

Like the insights from U.S. handgun production, reading this online has an additional benefit: more data. Keep scrolling to see a more expansive list of the top U.S. long-gun and misc. firearm producers from 2023.

U.S. Long-Gun Production (2023)

Total includes all U.S. manufacturers.

U.S. Misc. Firearms Production (2023)

Total includes all U.S. misc. firearm manufacturers.

*Per ATF, miscellaneous firearms are defined as: “Any firearms not included in the other categories, such as frames or receivers, etc. that are not identified as particular firearms.”

(Editor’s Note: Misc. firearm production total not factored in the “Top 40 U.S. Firearm Manufacturers” and “Top Exporter” charts.)

6. U.S. Firearm Exports

Year-over-year, U.S. firearm exports dropped in 2023 — from 548,196 to 473,638 (13.6%). The total observed in 2023 outpaced 2021 (450,342). Shotguns was the only category to record a YOY jump over 2022, rising from 43,312 to 45,067 (4%).

With 78,247 firearms exported, SIG SAUER reclaimed its status as the top U.S. exporter, a position it held in 2020 and 2021.

Ruger was the second-largest U.S. exporter (66,901), a ranking it has held every year since 2019.

After appearing as the top U.S. exporter for the first time since 2013 in 2022, GLOCK fell two places to the third-largest U.S. exporter with 64,832 firearms exported.

The top 60 U.S. firearm exporters are highlighted in the chart below.

Top U.S. Firearm Exporters (2023)

Total includes all U.S. firearm exporters. Editor’s Note: Misc. firearm exports are not included in totals. The top 2023 misc. firearms exporters were O.F. Mossberg Maverick Arms (2,757), Aero Precision (577), UB Exports (547), BP Firearms Co. (300), Kelbly’s Inc. (206) and Southern Ballistic Research (200).

7. U.S. Firearm Imports

Reading through some of SI early issues, writers would often scoff at foreign-made guns entering the U.S. marketplace. My, how things have changed.

According to the data supplied by the U.S. Census Bureau, there were 5,845,019 firearms imported into the U.S. in 2023. Because the data is updated monthly, 2024’s figures are also readily available — which revealed imports fell 7.4% to 5,412,509.

Unfortunately, the data doesn’t show which manufacturers/importers brought these firearms to the U.S. It does, however, provide country-level analysis. The top handgun-importing countries in 2023 were Austria, Brazil and Germany. In 2024, Turkey replaced Germany in the top three with significant annual growth (from 433,621 to 538,606).

Rifle imports fell slightly from 2023 to 2024 (from 1,120,219 to 1,022,109). Brazil, Canada and Spain made up the top three importing countries in 2023, while Turkey claimed the top spot in 2024, followed by Brazil and Canada.

Contrary to handgun and rifle imports, shotgun imports experienced an increase in 2024, rising from 979,853 to 1,117,656. This also is the only firearms category where the international totals exceed those produced in the U.S., which has been the case since 2020, according to our figures.

In each of the past two years, Turkey (662,761 and 797,361) and Italy (220,820 and 216,261) were the top two shotgun-importing countries by a substantial margin. The third-largest importing countries in 2023 and 2024, Brazil and China, imported 58,798 and 49,722 shotguns, respectively.

The country with the most imports over the past two years was Turkey, with 2,751,368 firearms imported into the U.S. across 2023 and 2024. Austria (2,150,935) and Brazil (1,764,190) round out the top three importing countries from 2023 and 2024.

U.S. Handgun Imports 2023 & 2024

Import data provided by the U.S. Census Bureau, Economic Indicators Division

U.S. Rifle Imports 2023 & 2024

*NESOI: “Not Elsewhere Specified Or Included” — Economic Indicators Division, U.S. Bureau of Census

U.S. Shotgun Imports 2023 & 2024

*NESOI: “Not Elsewhere Specified Or Included” — U.S. Census Bureau, Economic Indicators Division

2024 AFMER On Tap Next

The ATF will release its interim 2024 AFMER figures later this year, which features totals per category only. The full report, including breakdowns by licensed manufacturer, will be published at the beginning of 2026.

It’s certainly a “labor of love” putting this report together, but it’s one we’re proud to do in our efforts to better serve and educate you, our reader.

If you have a comment or observation from this year’s report, we’d love to hear from you: editor@shootingindustry.com.